Technical Specification

Probabilistic Multi-Adapter Heuristic System

1. System Description

Technical classification: Multi-Adapter Heuristic Ensemble with

correlation suppression, adversarial filtering, and computational resilience. Runs entirely

in the browser using public exchange data.

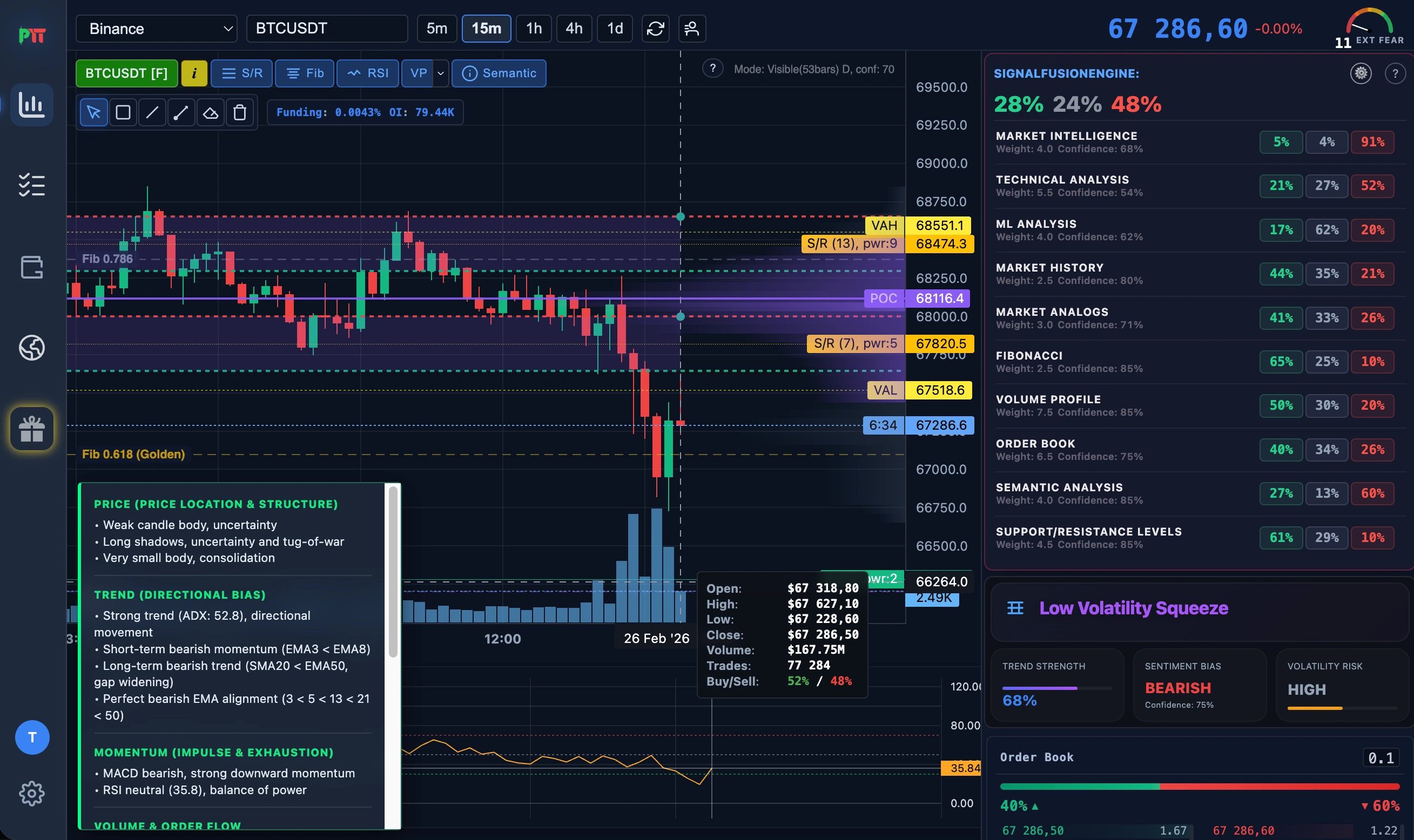

The system does not seek one correct indicator. It assembles 10 independent analytical computations and identifies where their outputs converge. Convergence across structurally different analytical methods produces higher-confidence readings than convergence within a single method applied multiple times.

What It Produces

A probability triplet (Growth / Fall / Consolidation) derived from weighted adapter outputs, calibrated against historical frequency distributions.

What It Does Not Produce

Entry and exit points, position sizing, stop-loss levels, or any form of trading recommendation. The output is a structured reading of current market state — its use is the trader's responsibility.

Layer 0 — Data Engineering

WebSocket + REST hybrid. 1000-candle REST initialization, OpenTime-validated WebSocket incremental updates. Conflict discard on duplicate or out-of-order bars.

Fault Tolerance

- Exponential Backoff (2n, cap 30s) — prevents API rate-limit bans on reconnect

- Heartbeat monitoring — detects WebSocket health degradation before data gaps occur

- Automatic candle resync — reconciles local candle state vs. exchange state after recovery

calibrate(raw, config) {

if (!this.isValid(raw)) return null;

return {

timestamp: this.syncClock(raw.openTime),

open: this.round(raw.o, config.pricePrecision),

high: this.round(raw.h, config.pricePrecision),

low: this.round(raw.l, config.pricePrecision),

close: this.round(raw.c, config.pricePrecision),

volume: this.truncate(raw.v, config.volPrecision)

};

}Layer 1 — Feature Extraction

~90 analytical signals computed from synchronized candle data. No absolute prices — only relative values: deviations, ratios, normalized slopes. This enables the model to run across different assets without scale bias, but it does not make the model universal.

Multicollinearity Risk

Indicators within the same family (e.g., multiple momentum oscillators) are correlated. Same-family adapter alignment is penalized by 0.45× to prevent redundant confirmation.

Normalization

P(Growth) + P(Fall) + P(Consolidation) = 1. This is a

mathematical constraint, not a statistical proof. The values represent conditional

historical frequencies.

Signal Penalty Logic

const PENALTIES = {

COUNTER_TREND: 0.65, // Price < EMA while Bias is Bullish

DEEP_DISTRIBUTION: 0.70, // SellVolume > 65% during Bullish Bias

CMF_DIVERGENCE: 0.80, // Money Flow != Price Direction

OVEREXHAUSTION: 0.78 // RSI > 72 while buying

};

confidence *= (bias === 'BULLISH' && rsi > 72) ? 0.78 : 1.0;Layer 2 — Context & Regime Engine

Classifies market state before adapter synthesis. The regime classification changes adapter weights — it does not change what individual adapters compute. Detection is lagging by design; the classification describes the current state, not the future state.

Regime Definitions

Chaotic

ATR_Percent > 4.5. Structure-dependent adapters (Structural Level Engine, Fibonacci Structure Model) receive reduced weight. Global confidence cap applied.

Squeeze

BB_Width < 0.10. Directional signals across all adapters are throttled. The system acknowledges that breakout direction is statistically uncertain in this state.

Trending

EMA stack alignment + ADX > 25 + slope/ATR > 0.08. Trend-following adapter weights are increased. Mean-reversion and oscillator signals are suppressed.

Consolidation

Neutral ATR, flat ADX, bounded structure. Oscillator and structural boundary signals receive higher weight. Momentum signals are down-weighted.

Kill Switch: Confidence below 30% → forced NEUTRAL output. No directional reading is emitted.

Layer 3 — Multi-Module Ensemble

10 structurally independent modules. Each consumes a distinct feature subset and applies distinct logic. Failure or degradation of any single module changes the weighted output — it does not prevent the remaining modules from producing a reading.

Adapter Reference

Technical Signal Ensemble

Quad-Pillar (Momentum / Volume / Structure / Trend). 60-bar RSI + MACD Divergence. Timeframe authority 0.6×–1.2×. Confluence Bonus 1.3× on 4-pillar alignment.

Statistical ML Model

Random Forest + Isotonic Regression calibration. Out-of-distribution detection. Feature space: autocorrelation, log-returns, volatility clusters.

Historical Pattern Engine

Combinatorial sequence search. Benjamini-Hochberg FDR correction. Sequential structure matching, not visual pattern matching.

Market Analog Search

DTW in 8D feature space. Temporal stretching up to 1.5×. Top-3 analog path projections, weighted by historical resolution frequency.

Signal Interpretation Engine

Priority-weighted synthesis of ~90 analytical signals (weights 2–10). Confusion Veto: 40% penalty on momentum-vs-trend conflict.

Structural Level Engine

Symmetric Fractals + ATR-adaptive DBSCAN. PWR Score from touch frequency, volume rejection, SFP reactions. Dual-decay memory.

Fibonacci Structure Model

Fractal swing discovery (min range 1.5× ATR). Standalone harmonic model — independent probability mass from Technical Signal Ensemble Structure Pillar.

Volume Structure Analysis

AMT-based POC, VA, HVN/LVN analysis. Measures price acceptance geometry — structurally distinct from directional order flow.

Order Book Microstructure

Power-law depth decay (i−1.2). Wall at 3× average depth. Confidence gated at spread > 0.1%.

Market Regime Controller

Regime supervisor. Global Adversarial Penalty Matrix. Applies Signal Category Caps (35% limit) to prevent family-based over-weighting. ATR > 3.0% or BB-width < 0.10 → HOLD dilution. Entropy NEUTRAL override on consensus failure.

Layer 4 — Resilience

Exponential backoff (2n, cap 30s). Heartbeat monitoring. AbortController-scoped request lifecycle. Cache TTL 15–30s with symbol-change invalidation. Incremental indicator updates per tick. Analytical cycle throttled to 1000ms.